How To Pay Off Credit Card Debt Fast

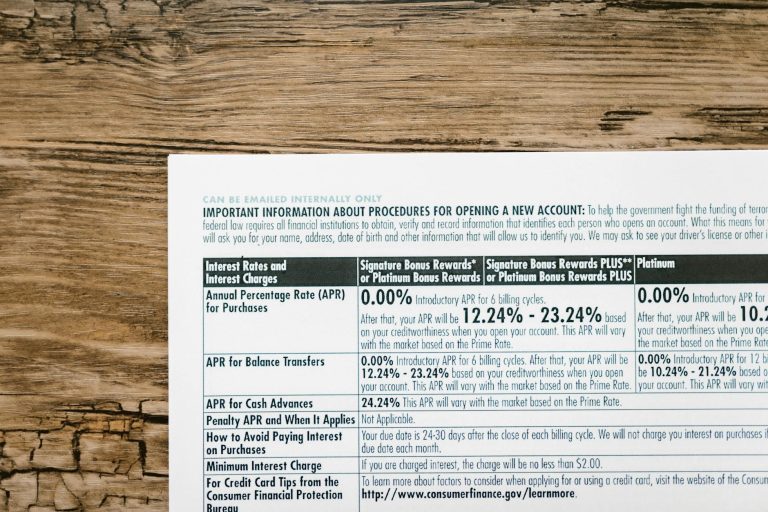

Credit card debt has become a defining financial issue for millions of Americans, with the average cardholder carrying over $6,000 in balances (Source: Federal Reserve). The problem is compounded by high interest rates, which can exceed 18% as of March 2026 (FRED), turning small purchases into costly obligations. For example, a $500 purchase at 18% APR would cost over $600 in interest alone if left unpaid for two years. This is not just a personal finance issue—it’s a systemic challenge tied to broader economic trends. The Federal Reserve’s recent hikes to the federal funds rate, now at 3.64%, have pushed credit card rates to historic highs, mirroring the 30-year mortgage rate of 5.98% (FRED). Inflation, currently at 2.2% (BLS), further erodes purchasing power, making it harder to allocate funds toward debt repayment.

The stakes are clear: credit card debt is a major contributor to financial stress, with 1 in 4 households reporting medical debt or credit card debt as their largest financial burden (Source: Consumer Financial Protection Bureau). For those struggling to break the cycle, the path to freedom requires more than good intentions—it demands strategic planning. The key lies in understanding how high-interest debt accumulates and how to prioritize repayment in a market where even low-risk investments like Treasury bonds yield 4.06% (FRED). This is not a problem that can be solved by saving more or earning more; it requires a deliberate, data-driven approach.

Strategies to Pay Off Credit Card Debt Fast

The most effective way to eliminate credit card debt is to prioritize paying off the highest-interest balances first, a method known as the “avalanche approach.” This strategy targets the most expensive debt first, reducing the total interest paid over time. For example, if you have two cards—one with 18% APR and another with 15%—paying off the 18% balance first saves hundreds in interest. Conversely, the “snowball method” focuses on paying off the smallest balances first to create momentum, which can be psychologically rewarding for those overwhelmed by debt. Either approach is valid, but the avalanche method is mathematically superior for minimizing long-term costs.

To implement this strategy, start by listing all credit card balances, their interest rates, and minimum payments. Use a spreadsheet or a budgeting app like Mint to track progress This ensures that you’re not just paying the minimum but aggressively reducing principal. The goal is to make all payments above the minimum, which can be challenging but is essential for accelerating debt elimination.

Another critical step is to avoid new debt while paying off existing balances. This means resisting the urge to charge more to cards, even for emergencies. Instead, build an emergency fund of 3–6 months’ expenses using a high-yield savings account (Source: Bankrate). With the current 10-Year Treasury Yield at 4.06%, even a small emergency fund can earn passive income, reducing the need to rely on credit cards. For example, $5,000 in a high-yield account could earn $202.50 in interest annually, which can be used to make extra payments.

Leveraging Current Market Trends to Your Advantage

The current economic environment offers unique opportunities for those seeking to pay off credit card debt. For instance, the Federal Reserve’s aggressive rate hikes have pushed credit card rates to near historic highs, but this also means that low-risk investments like Treasury bonds or CDs are yielding 4.06% (FRED). This creates a paradox: while credit card debt is expensive, alternative investments may offer better returns. However, these opportunities are not easily accessible to everyone. Most consumers lack the capital or knowledge to invest in Treasury bonds, which require a minimum investment of $1,000.

That said, there are still ways to use market trends to your advantage. For example, the current 10-Year Treasury Yield of 4.06% (FRED) is higher than the average credit card rate, meaning that even a small amount invested in low-risk assets could generate more income than the interest paid on debt. For instance, $10,000 in a Treasury bond would earn $406 in interest annually, which could be used to pay down credit card debt. However, this requires discipline and a willingness to prioritize long-term gains over short-term spending.

Another opportunity lies in refinancing. While credit card refinancing is not as common as mortgage refinancing, some card issuers offer balance transfer options with 0% APR for a limited time. For example, a 0% APR offer could save hundreds in interest if used strategically. However, these offers often come with fees (typically 3–5% of the transferred amount) and a limited promotional period, so they should be used sparingly and only for debt with higher rates.

Tools and Resources to Accelerate Debt Repayment

The right tools can make a world of difference in paying off credit card debt. Budgeting apps like YNAB (You Need A Budget) or PocketGuard can help you track expenses, allocate funds to debt repayment, and avoid overspending. These apps often integrate with credit card accounts, providing real-time insights into spending habits. For example, YNAB’s zero-based budgeting approach forces you to assign every dollar a job, ensuring that debt repayment is a priority.

Another valuable resource is a high-yield savings account, which allows you to earn interest on your emergency fund while keeping money accessible for debt payments. With the current 10-Year Treasury Yield at 4.06%, even a modest savings account can generate passive income. This strategy is particularly effective for those who struggle with impulse spending, as it creates a financial cushion while reducing reliance on credit cards.

Financial advisors can also play a crucial role in developing a personalized debt repayment plan. A certified financial planner can help you assess your financial situation, set realistic goals, and create a roadmap for eliminating debt. For example, if you have a complex debt structure or multiple credit cards, a financial advisor can recommend strategies like debt consolidation or refinancing. However, it’s important to choose a reputable advisor, as the financial industry is rife with scams. Look for advisors who are certified by the CFP Board and have a strong track record of helping clients achieve their financial goals. 5 Signs You Need A Financial Advisor covers this in more detail.

Challenges and Pitfalls to Avoid

While paying off credit card debt is achievable, it’s not without its challenges. One of the most common pitfalls is the temptation to use new credit to cover existing debt. This not only increases the total amount owed but also extends the repayment period. For example, if you transfer a $5,000 balance to a card with a 0% APR offer, you might be tempted to use the same card for a new purchase. This creates a cycle of debt that’s harder to break.

Another challenge is the psychological toll of debt repayment. The stress of managing multiple payments and tracking expenses can be overwhelming, especially during economic uncertainty. For instance, with the current unemployment rate at 4.3% (BLS), many households are already stretched thin, making it harder to allocate funds to debt. To mitigate this, it’s essential to build a support system. This could include financial advisors, support groups, or even a trusted friend who can help keep you accountable.

Finally, there’s the risk of overextending yourself. While it’s tempting to allocate all available income to debt repayment, this can lead to burnout. A balanced approach is necessary—allocate a portion of your income to debt, another portion to savings, and the rest to needs and wants. This ensures that you’re not sacrificing your quality of life while paying off debt.

Conclusion: A Path to Financial Freedom

Paying off credit card debt is not just about numbers—it’s about creating a sustainable financial strategy that aligns with your goals and circumstances. By leveraging the current economic environment, using the right tools, and avoiding common pitfalls, you can take control of your finances and move toward long-term stability. The key is to start today, not wait for the perfect moment. Whether you choose the avalanche method, snowball method, or a combination of strategies, the goal is the same: eliminate debt and build a foundation for financial freedom.

In a world where inflation and interest rates are shaping every financial decision, the ability to pay off debt quickly is a powerful tool. By staying informed, using data-driven approaches, and staying disciplined, you can turn the tide against credit card debt and reclaim control of your financial future. The road to freedom is paved with small, consistent steps—and every payment you make is a step closer to that goal. How Credit Shapes Your Financial Future in 2026 covers this in more detail.